LTC Bullet: Five Things You Probably Don’t Know about Long-Term Care Friday, May 2, 2025 Seattle— LTC Comment: What if most of what we think we know about long-term care is wrong? Let’s explore some possibilities after the ***news.*** *** WEDNESDAY, I participated in an “Alliance for Health Policy” event in Washington, DC. The Alliance’s annual Signature Series addresses challenging issues in health policy “by convening cross-sector dialogue with experts in both policy and practice” to “critically examine and identify what’s at stake, as well as key areas of opportunity.” Last year’s theme focused on the transformative power of Artificial Intelligence (AI) in health care and health policy. This year’s theme is “aging.” Participants imagined what it would be like to be 80 years old (easy for me) and considered what challenges being that age could bring to various demographic scenarios. I’ll be back

in DC next week for Genworth and CareScout’s Symposium on “Sustainable

Solutions: The Future of Long-Term Care Financing.” Check out the

program’s landing page

here, where you can read about each of the four panels and review the

panelists’ bios. Join us virtually for the Symposium

here. I’ll be on Panel #4: "Better Together..." – Public + Private

Collaboration. Expect some spirited discussion. *** LTC BULLET: FIVE THINGS YOU PROBABLY DON’T KNOW ABOUT LONG-TERM CARE LTC Comment: Will Rogers is famously quoted as saying, "It isn't what we don't know that gives us trouble, it's what we know that ain't so." No truer words have been spoken about long-term care. Here are some thoughts and considerations on that theme. I may develop these notes into a paper, but for now just see what you think and feel free to offer feedback to smoses@centerltc.com. “Five Things You Probably Don’t Know about Long-Term Care” by Stephen A. Moses

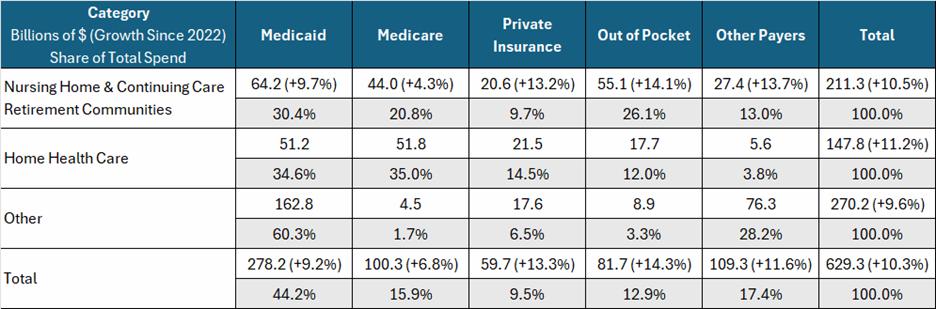

a. $97 trillion wealth in … i. Retirement savings ($40T), ii. Home equity ($35T) iii. Life insurance ($22T) b. LTC spending: $629.3B i. Medicaid: $278.3B, 44.2% ii. Medicare: $100.3B, 15.9% iii. Private insurance and other public payers: $169.0, 26.9% iv. Out of pocket: $81.7B, 12.9% 1. Half is income of people already on Medicaid a. Mostly Social Security income b. But pension and other private income too 2. Only half could be spend down of savings a. $40.9B, 6.5% b. $1 out of $15 spent on LTC

a. Medicaid treats the affluent well i. High income people qualify (medically needy) ii. High asset people qualify (exempt wealth) iii. Affluent people get the best Medicaid offers 1. Key money iv. Medicaid is a windfall for affluent heirs 1. Big exemptions 2. Little estate recovery b. Medicaid treats the poor poorly i. Few assets wiped out quickly ii. Lack key money, so … 1. Shunted to the worst, high-Medicaid nursing homes and home care providers iii. Victims of “LTC racism”

a. Since ACA, Obama Care, in 2010 i. 90% federal match; $9 federal for every $1 state ii. Covers working age adults with incomes up to 138 percent of the federal poverty level iii. Mostly single, often unemployed, childless people incentivized to remain so and to attract others to the same generous benefit b. Expansion population grew from nothing to 20% of Medicaid dollars c. Aged and disabled i. Went from 25% of enrollees and 69% of expenditures (2003) ii. To 20% and 50%, respectively (2023) d. Dual eligibles i. From 14% and 42% (2005) to 14% and 32% (2023)

a. Diametrically contradictory public policies i. Reward accumulation of wealth, such as tax-favored IRAs and 401(k)s that build nest eggs; subsidized mortgages and mortgage-interest tax deductions that grow home equity; and tax-deferred growth and tax-free death benefits that boost life insurance cash value. ii. Medicaid eligibility policies that discourage spending for LTC 1. Punish the poor 2. Reward the affluent. b. Results i. Plenty of private funds in the economy lie fallow for LTC financing 1. Less full price revenue for LTC providers 2. LTC access and quality suffer ii. As those funds are not at risk, LTC insurance market to protect them lags 1. People ignore LTC until they need it 2. Then qualifying for Medicaid is the path of least resistance iii. Too many people rely on Medicaid, with dire consequences 1. Poor reimbursements a. Caregiver shortages b. Deficient care c. Too little HCBS d. Nursing home closures 2. Institutional bias a. Decades warehousing elderly in nursing homes b. Still problem in rural areas 3. Discrimination a. In favor of private payers i. Key money ii. Access to best institutional and home-based care b. Against Medicaid recipients i. LTC racism ii. Condemned to high-Medicaid, poor quality care 4. Moral hazard a. Easy access to Medicaid caused … b. Complacency, resulting in … c. Failure to plan, save, invest or insure in LTC

a. Medicaid must pay market rates i. Eliminate discrimination against poor and for affluent ii. LTC providers pay adequate wages 1. Solves caregiver shortage 2. Ensures caregiver quality iii. Competition 1. For private payers 2. Instead of begging for more Medicaid iv. But Medicaid cannot pay market rates with so many on the program 1. Must reduce Medicaid census 2. Increase private financing a. Put $97 trillion private wealth to work b. Attract LTC insurance to protect the wealth b. Solutions to reduce Medicaid dependency and attract private wealth to LTC i. Keep Medicaid treatment of income the same 1. Continue to require income spend down for care (medical or LTC) 2. Excess Social Security, pension and other private income offsets Medicaid costs 3. But LTC providers receive market rates, not Medicaid’ previous below-cost rates i. Stop allowing spend down by purchasing exempt assets (“Medicaid's $100+ Billion Leak”) 1. Asset spend down does not have to be for care costs currently a. Unlike income spend down b. Allows conversion of unlimited countable wealth to exempt status 2. So make them the same a. Potential savings of $100+ billion per “class” of elders i. New “class” of infirm elders every two or three years iii. Eliminate or radically reduce Medicaid’s huge home equity exemption 1. Let seniors’ $14 trillion of home equity flow into LTC financing 2. Vast new revenue potential for LTC providers 3. Better access and quality 4. Strong incentive to insure home equity early against LTC cost iv. End abusive Medicaid planning methods that benefit only the affluent 1. Irrevocable trusts 2. Medicaid compliant annuities v. Extend Medicaid’s five-year lookback to 10 years or 20 1. Easy to check through assessors and recorders 2. Discourages early planning for Medicaid LTC vi. End systemic LTC racism 1. When all funders, including Medicaid, pay market rates … 2. Discrimination based on payment source will end, and 3. LTC racism will disappear. vii. End Obama Care preference for able-bodied, working-age adults 1. Stop 90% match for “expansion” population 2. Give Medicaid back to the vulnerable poor, aged and disabled people it was intended to serve viii. Let states experiment 1. Block grants a. Accept less federal money b. Receive more policy flexibility 2. Experiment with creative ways to do more with less a. States as laboratories of federalism |