LTC Bullet: Dog Bites LTCI Friday, February 27, 2015 Seattle— LTC Comment: A critically important positive report on LTC insurance got short media shrift while a poor academic hit job swept the wires. Today’s LTC Bullet sets the matter straight.

LTC BULLET: DOG BITES LTCI LTC Comment: “Good news” is an oxymoron. “Bad news” is redundant. If it bleeds, it leads. In today’s guest column, author-adviser Stephen D. Forman explains why the much-ballyhooed Boston College (BC) “man-bites-dog” critique of private long-term care insurance over-shadowed a more thoughtful and accurate “dog-bites-man” monograph by LifePlans. Read today’s Bullet and you’ll get the reference. Two LTC Bullets already dismembered BC’s “Long-Term Care: How Big a Risk” analytically. See “LTC Bullet: How Careless Economists Boosted LTC Risk” and “LTC Bullet: When Bad Models Happen to Good People,” the latter piece also authored by Mr. Forman. What we have not done until now is give comparable attention to LifePlans’ superior analysis of the benefits and impact of long-term care insurance. The following article corrects that oversight. Full disclosure: Stephen D. Forman and the LTC insurance marketing company he and his brothers run are long-time supporters of the Center for Long-Term Care Reform. They publish a very thoughtful occasional newsletter called “Your Next LTCA Sales Idea.” Much more than “salesy” fluff, that publication appeals to an LTCI producer’s intellect. It arms him or her with solid information and analysis to persuade reluctant prospects who’ve been misled by careless scholars and lazy journalists. We thank the Formans for permission to share Stephen’s essay with you today. [N.B.: Much of the highlighted material in the following article was not bolded in the original LifePlans’ publication quoted.]

"Dog Bites Man" It's a shame a recent dour model by the Center for Retirement Research went viral at the same time LifePlans, Inc. published its landmark report, "The Benefits of Long-Term Care Insurance and What They Mean for Long-Term Care Financing." Although the latter publication is one of the most defining pieces of positive news for our industry in the last decade, I can't think of a major news outlet which covered it.¹ Synthesizing novel research with that of the US Dept of Health & Human Services, the SCAN Foundation, the Mature Market Institute and America's Health Insurance Plans, the study is an update of similar work conducted in 2002. Divided into three parts, it looks first at the impact of long-term care insurance on policyholders, then its impact on family and caregiving, and finally its impact on Medicaid.

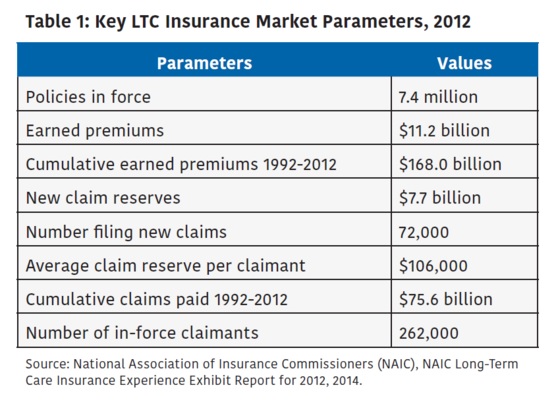

LTCI: POLICYHOLDERS The "face value" of all LTCI policies payable stands at $1.98 trillion. Since not everyone will claim-- or claim in full-- the industry is expected to ultimately pay out $679 billion on the current in-force book. For some context, the country as a whole spent $208 billion on long term services and supports in 2010. Although LTCI has been dogged by a scurrilous "use it or lose it" accusation of late, the LifePlans study concludes, "LTC insurance policies provide high value in benefits relative to premiums paid." In support, the authors model a 60-year old who pays premiums through age 82 (on a statistically representative policy), then show how 22-years of premium payments would quickly be returned after just 5 months on claim. By comparison, a 60-year old without insurance would have to set aside $1,666 each month (at 2% interest) to achieve what our LTCI policyholder can leverage with just $188 per month. In a first, the researchers then confront the "rate increase" argument, building-in a 30% increase in year 7 in one scenario, and a 50% increase in year 7 in another to determine whether the policy still provides good value. It turns out, such rate actions barely move the dial: in the former case, 22-years of premiums are returned after just 6.6 months on claim; in the latter, just 7.3. Finally, for good measure the researchers examine self-funding-- and quickly dismiss it. "While savings do not cover even average costs, insurance covers catastrophic situations, when much more than the average duration of care is needed."

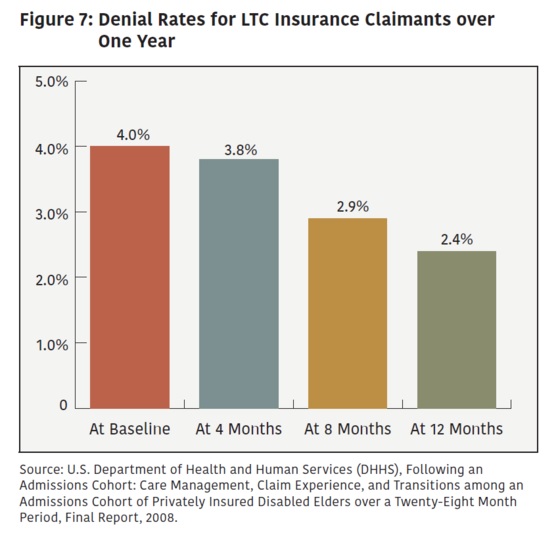

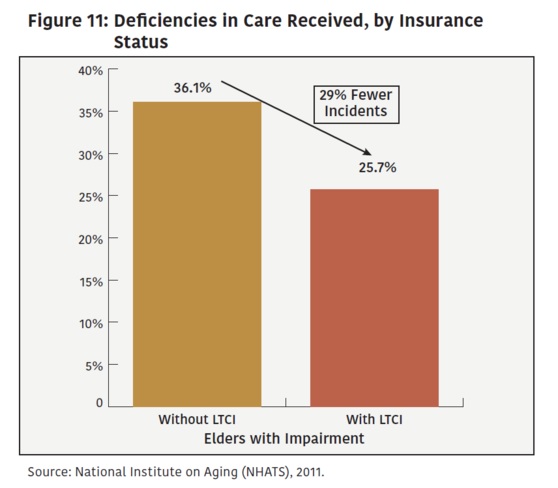

LTCI: FAMILY Wade into any online forum and you're sure to find them: sign-waving demonstrators telling anyone who will listen, "Insurance companies are crooks!" Even when the carrier makes good on a $700,000 claim we're told they "build up a wall and make it difficult." As LTCI producers, we've subjectively known the opposite to be true, but now LifePlans categorically rebuts such slander once and for all. According to the report, "Almost all who filed a claim at baseline were either approved or awaiting final decision. When claims were denied, it was usually (as was to be expected) because the claimant did not meet policy benefit eligibility criteria." Furthermore, the process is easy: policyholders "do not feel they have to 'fight for' benefits," and by a landslide (94%) interviewees report no disagreements with their insurance companies-- or that their disagreements were resolved to their satisfaction. (For context, here's a headline I wrote last year: "LTC Insurer Declines 41% of Claims. Oops! I Meant TN Medicaid.") The positive impact of these claims on the insured and her family can be profound. Those with insurance receive 35% more care than those without. Likewise, those with insurance report almost 1/3rd fewer incidences of unmet or under-met needs (eg wetting of clothes, going without bathing, or having to stay in bed) than their uninsured counterparts. Research from the study also shows that individuals caring for elders with LTCI are "nearly twice as likely" to be able to continue working than elders without insurance. Family caregiving hours are also reduced by about 10%, which allows caregivers to focus on companionship and social interaction rather than hands-on care. "This helps restore a greater sense of normality to the relations between adult and children... or between spouses." As we've been promoting within the industry for years, care coordination (to help locate and arrange the most suitable services) is described as "highly valued."

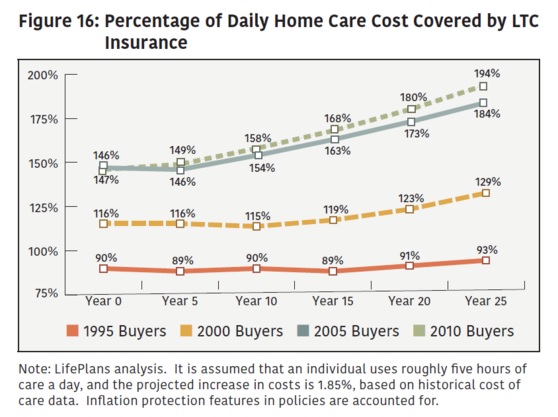

LTCI: MEDICAID Medicaid pays for two of every three dollars of LTC costs in America. Like two sides of a scale, we understand there's an implicit relationship between public and private financing-- now the study helps quantify it. By creating a simulation taking into account socio-demographic profiles, state-specific Medicaid rules, a policyholder dataset, historic trends in assets and income, and claims experience, the researchers estimated "spend down" rates both with and without LTC insurance. What they found is that LTC insurance reduces the likelihood of spend down between 47 - 65% among nursing home claimants. (Looking at other settings like assisted living and home health care, "spending down is much less likely than in a nursing home, and for those with LTC insurance it is virtually eliminated.") From a policy perspective, we must turn to the big picture. Does encouraging the purchase of private LTC insurance make good sense? The LifePlans study concludes that each inforce policyholder will save Medicaid $6,681 over her lifetime. Multiply this over the current cohort of policyholders and we're looking at a savings of $49.4 billion. Part of the reason LTCI is so effective is that it covers so much of the cost of care. Buyer cohorts from 1995 through 2010 were reviewed through their first 25 policy years. LifePlans found that 93 - 194% of home care costs were covered, as were 107 - 128% of assisted living costs, and 50 - 79% of nursing home costs. (Here they used average policies and average costs.) In a separate trial, the claims of actual policyholders were studied at four, eight, twelve and sixteen month intervals. At any given point, between 69 - 75% of these policyholders were receiving "most or all" of the cost of care reimbursed by their policies. The researchers are favorable once again: "In the service settings most highly desired by individuals with impairments-- home care and assisted living-- insurance should cover almost all of the daily costs of care for a typical policyholder." Meanwhile, nursing facility coverage is "not out of line with cost-sharing required by health insurance plans and is also consistent with expectations of individual buyers, who indicate that they expect their policies to pay for most but not necessarily all of the costs of care. They choose to accept this cost-sharing in part to keep premiums down."

A TALE OF TWO STUDIES According to the CDC, nearly 4.5 million Americans are bitten by dogs each year. When the expected happens, it's not newsworthy. It no more surprises us than the $20.5 million in routine, clockwork claim payments made by our country's long-term care insurance carriers each and every day. There's just no headline there. On the other hand, when "man bites dog," that's shocking and absurd. As Dr. Christopher Bader of Chapman University explains, "People often don't realize that when they're watching the news they're watching the worst possible scenario. That's why it's news: A serial killer gets airtime because he's rare, not because serial murders are on the rise." Why should coverage of LTCI break these rules? The sensational rises to the top, while the mundane gets passed over. And the Center for Retirement Research story was very sensational. Not only did the CRR model try to upend conventional wisdom, but it teased us of bigger shoes still to drop. And in true "man bites dog" fashion, some of our nation's leading personal finance columnists began considering Medicaid as a legitimate first-look LTC solution for their readers. Meanwhile, the LifePlans report is simply quiet good news about a solution that works. It not only demonstrates Medicaid cost savings (leading to program stability), but also better outcomes for those served. It's not sexy, and it doesn't take on the establishment. Would it be gratifying if the media ran the LifePlans story? Of course it would! It would be a great service to their readers-- a duty, really, and a responsibility to present the other 99.99% of the news. Until then, we must be our own bullhorns. It's incumbent upon each of us to focus on the positive, both in our lives, our professions, and for the industry of long term care to which we devote ourselves so passionately. Our clients and policyholders deserve nothing less from us. ¹ I acknowledge that some readers will be familiar with the LifePlans (AHIP) report since it has been breathlessly recirculated within our own tightknit LTC community. Still, few reviews have gone beyond the Executive Summary. Mr. Forman is co-author of "The Advisor's Guide to Long-Term Care" (2nd Ed.) published by National Underwriter, and a regular contributor to LifeHealthPro and ProducersWEB. Reach him at steve@ltc-associates.com. |